(Image credit: Intel)

-

Facebook -

X -

-

-

Pinterest -

Flipboard -

Email

Get Tom's Hardware's best news and in-depth reviews, straight to your inbox.

You are now subscribed

Your newsletter sign-up was successful

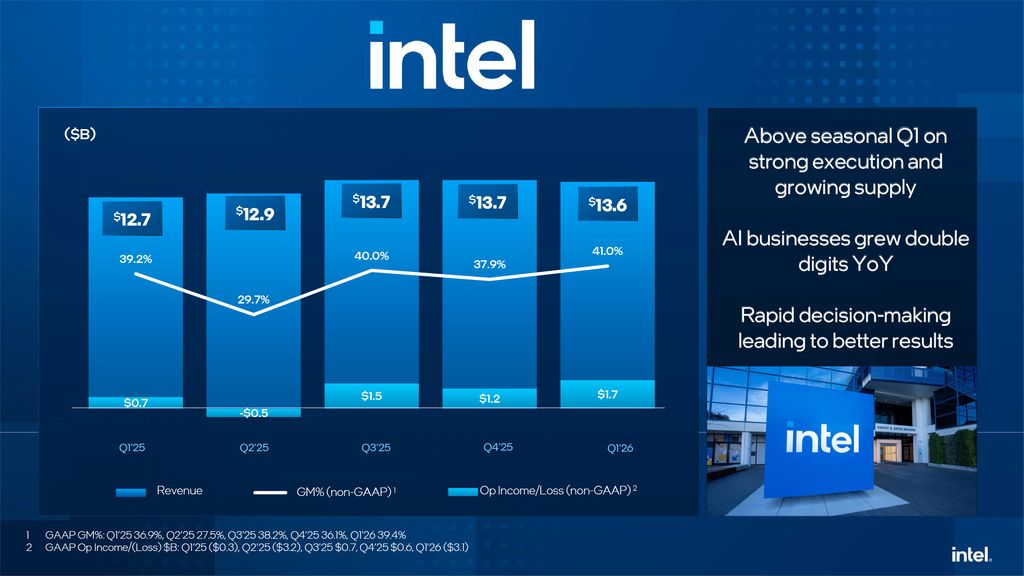

Intel on Thursday published its financial results for the first quarter, and its stock rocketed 28% in after-hours trading, hitting an all-time high of $80.01. The results saw Intel significantly beating its own outlook by $1.4 billion due to rising demand for data center-grade CPUs, decent demand for client products, and increased output and productivity at Intel's own fabs. Despite results that are well above seasonality, the company still posted a rather massive $3.7 billion loss as it wrote down Mobileye goodwill and restructuring charges. However, the results can be considered positive as on a non-GAAP basis, the company recorded $1.5 billion in net income.

"We delivered robust Q1 results, reflecting the growing and essential role of the CPU in the AI era and unprecedented demand for silicon, as well as our disciplined execution to expand available supply," said David Zinsner, Intel CFO. "We remain focused on maximizing our factory network to improve available supply and meet our customers’ needs throughout the year."

(Image credit: Intel)

In the first quarter of 2026, Intel earned $13.6 billion in revenue, up 7% year-over-year (YoY), and flat with the fourth quarter of 2025, meaning that the results are well above seasonality. The company's R&D and SG&A expenses totaled $4.4 billion, down 8% from $4.8 billion in the same quarter a year ago, whereas its gross margin increased to 39.4% from 36.9% in Q1 2025. In addition, Intel generated $1.1 billion in cash from operations. Nonetheless, the company recorded a $3.7 billion GAAP loss in the first quarter of 2026, up massively from $800 million in Q1 2025.

Article continues below

(Image credit: Intel)

However, the loss is a result of a $4.07 billion 'restructuring and other charge,' which includes a $3.447 billion (primarily) Mobileye goodwill impairment charge and $623 million restructuring and other charges. That said, the losses were largely driven by accounting charges required under GAAP, rather than weakness in Intel’s core product business, although the company’s foundry division continues to generate significant operating losses.

Intel Products: Better than before, worse than could have been

At a high level, Intel's product business is clearly stabilizing. Among improved demand, the company attributes its improved business results to higher output and productivity of its own fabs that make chips on its Intel 7/4/3 process technologies. Nonetheless, Intel admits that it cannot meet all the demand, which limits its growth.

(Image credit: Intel)

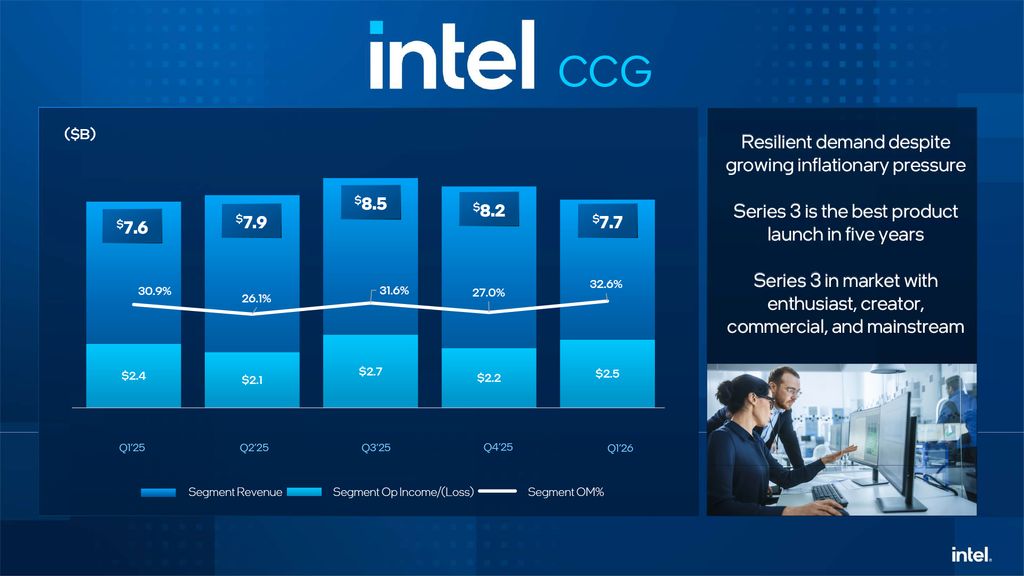

The Client Computing Group (CCG) generated $7.7 billion in revenue, $2.5 billion operating income, and 32.6% operating margin in Q1 2025, which is clearly up from $7.6 billion revenue, $2.4 billion operating income, and 30.9% operating margin in the same quarter a year ago. Keeping in mind that sales of PCs in the first quarter were affected by the turmoil on the DRAM and storage markets as well as demand outstripping supply (partly because Intel continues to shift some capacity from client to data center products) CCG's results can be considered good.

" Even with improved factory output demand outstripped supply against a client TAM that remains resilient despite industry-wide component shortages and inflationary pressures," Zinsner said. "Our AI PC revenue grew 8% sequentially and now represents greater than 60% of our client CPU mix."

(Image credit: Intel)

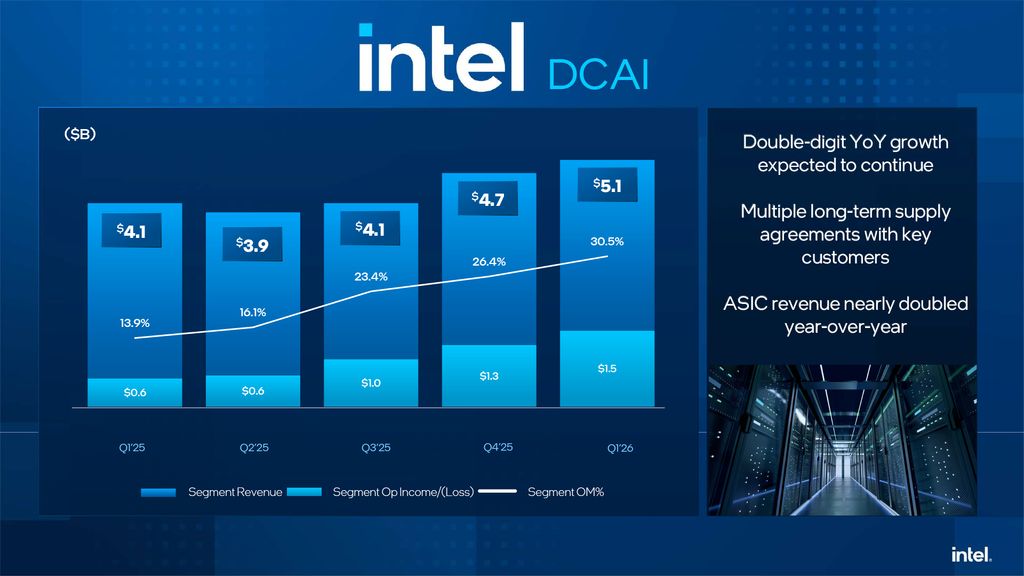

The Data Center and AI (DCAI) increased its earnings to to $5.1 billion, up 22% year-over-year and up $400 million quarter-over-quarter. Perhaps more importantly, the business unit's operating margin increased to 30.5%, and it generated $1.5 billion in operating profit (up from $0.6 billion a year before).

This growth reflects a meaningful shift in demand: hyperscalers are deploying more CPUs alongside accelerators as AI workloads move from training toward inference and agentic workloads. Intel claims this marks a structural change in the AI stack as CPUs reclaim their role in the data center and are set to increase attach rates per GPU, which remain primary compute engines. In addition, Intel cited yield and productivity improvements at its Intel 3-capable facilities that produce Xeon 6 processors as major factors for increased margins and profitability of DCAI.

(Image credit: Intel)

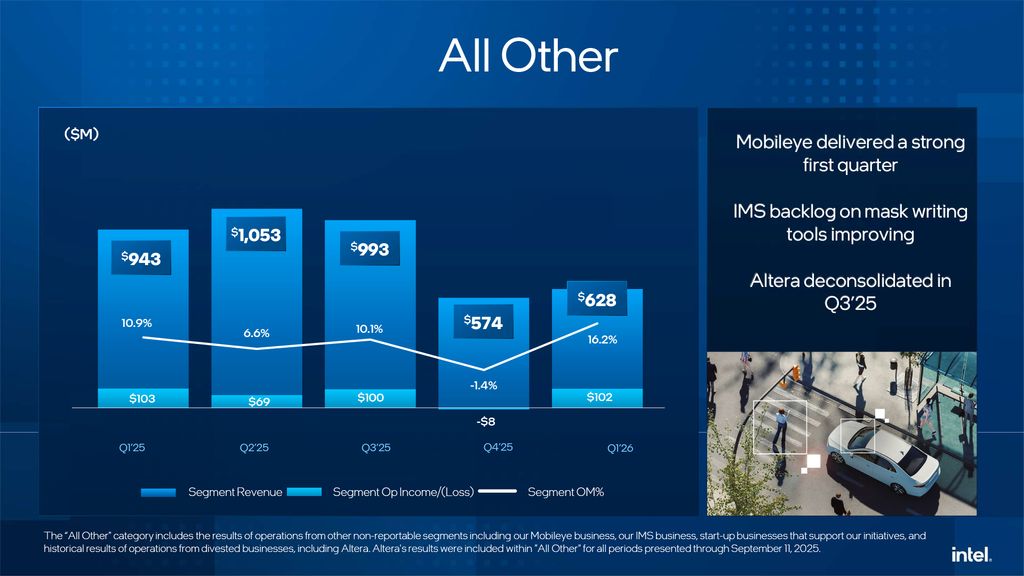

Intel's 'All Other' segment — which includes Mobileye and IMS mask writing services — remains small after deconsolidation of Altera in Q3 2025. During the quarter, its revenue totaled $628 million, down 33% year-over-year (largely due to the deconsolidation of Altera), but at the same time, the segment generated $102 million in operating income, which is good news as it lost $8 million in the previous quarter.

Intel Foundry: Produces gems, absorbs losses

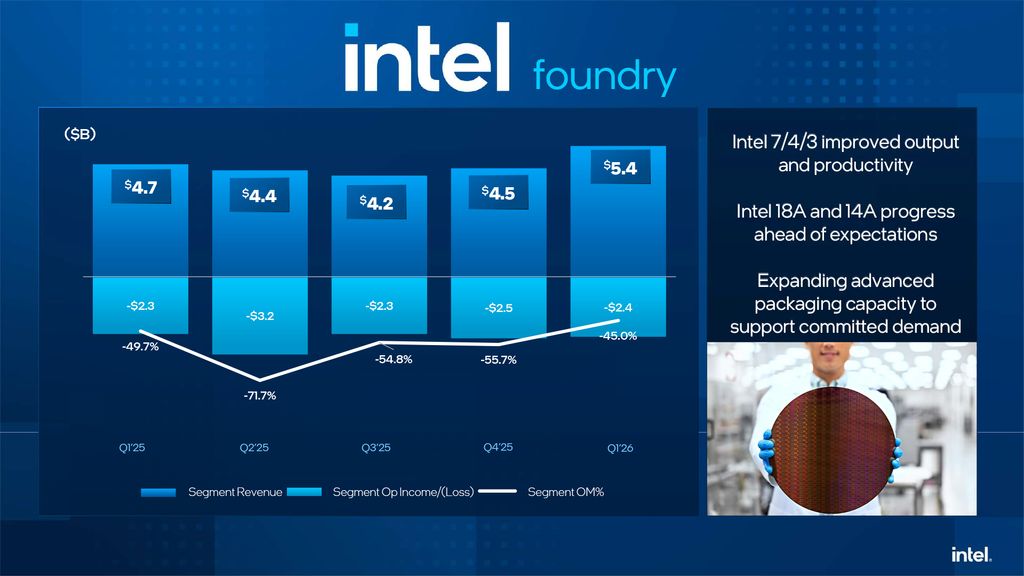

Intel's Foundry division produces the company's most profitable products for client and data center applications and also absorbs all the losses of the company. The division generated $5.4 billion in revenue last quarter (up from $4.7 billion in Q1 2025), but posted an operating loss of roughly $2.4 billion (up from $2.3 billion in Q1 2025), which means an operating margin near -45%.

(Image credit: Intel)

The current result reflects higher output (which drives revenue) as well as the early 18A ramp (which generates higher losses). Essentially, Intel Foundry absorbs the full cost of ramping 18A, including low yields, high depreciation, as well as heavy R&D spending on future nodes like 14A. While Intel highlighted improving yields across all of its latest nodes (7/4/3) and growing advanced packaging backlog, external foundry revenue remains minimal, and meaningful customer-driven volume is unlikely before late 2026 or 2027 with 18A or even later with 14A. One thing to keep in mind here is that EUV-based Intel 3/4/18A nodes still represent a minor share (over 10%, probably less than 20%) in Intel's total product mix, which leaves a lot of space for growth.

Intel's messaging during the conference call with investors and analysts emphasized Foundry's progress: better yields, improving factory output, and increasing customer engagement, including partnerships with companies like Google and participation in large-scale initiatives such as TeraFab. While these are important signals, they do not yet translate into financial success for the foundry business.

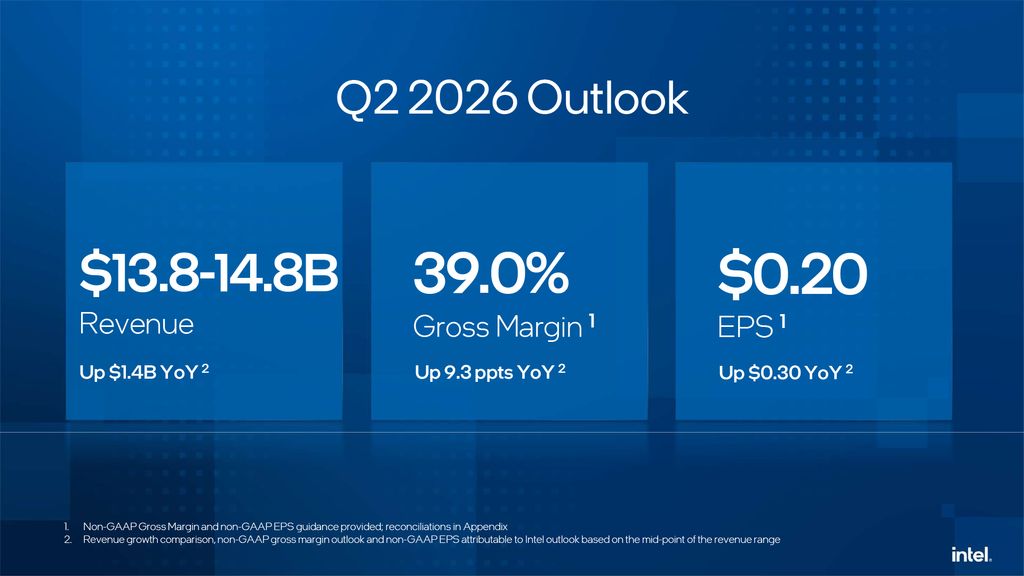

Q2 2026 outlook

Intel expects its second quarter of 2026 to show modest sequential growth and projects revenue to be from $13.8 billion to $14.8 billion and non-GAAP gross margin of 39%.

(Image credit: Intel)

The company's management expects demand for data center CPUs to remain strong, as well as demand for client processors to remain robust, as many PC makers have accumulated enough DRAM and 3D NAND for their systems. However, Intel warns that demand may outstrip supply and also says that in the second half of the year, memory and SSD supplys will be depleted, forcing PC makers to obtain their memory at spot prices, passing increased costs to consumers, which will hit PC sales. In addition, as Intel will increase output of its Core Ultra 3-series Panther Lake processors by six or seven times in Q2, its margins will take a hit.

Follow Tom's Hardware on Google News, or add us as a preferred source, to get our latest news, analysis, & reviews in your feeds.

-

C114 Communication Network

C114 Communication Network -

Communication Home

Communication Home